If you’re just launching your start-up business but don’t have a financial background, then you might not be sure where to start when it comes to recording your sales and purchases. Besides, you’re bound to be pre-occupied with establishing your brand, delighting customers and developing new relationships to generate growth.

The thing is it’s important to have an effective system in place to record all these activities in your organisation. This allows you to monitor accurately how well you're doing. The only way to achieve that is through an accurate and efficient record of business transactions through bookkeeping.

What kind of system you need to implement to achieve this will depend on the business you’re operating, your specific needs and where you’re at in the business lifecycle. Ultimately understanding your circumstances and reporting requirements will provide clarity as to how to best go about documenting this information.

The sales ledger is an account for every customer of a business and records the money received for products or services, plus what is still owed. This is then represented in the annual accounts, balance sheet as either accounts receivable or, trade debtors.

The purchase ledger is an account of the suppliers of a business, documenting from whom the organisation has made purchases, what’s been paid for, and how much is still owing. This is represented in the annual accounts, balance sheet as accounts payable or, trade creditors.

Quite simple really, it’s essential to have a system in place that processes all sales and purchases so that financial information is accessible on a regular basis. This then ensures you can monitor both performance and cash flow accurately. Without bookkeeping, creating management accounts would be a mundane task and producing your annual accounts would be near enough impossible!

As a start-up entrepreneur you’ll probably think that what you need to record appears quite basic. It’s just a case of keeping a tab of all your transactions, informing HMRC that you’re trading, and remembering to pay your tax and national insurance. Can't this be covered off by a simple spreadsheet? Unlikely!

Unfortunately you’d need to know exactly what you’re doing. If you do, great. If you don’t, then you should understand that knowing when to record certain things, how they should be treated and why, is anything but a simple process. It’s also very time consuming.

Even if you did get a grasp of bookkeeping eventually, you might well still miss opportunities. For example, there are certain allowable business expenses that you can claim for against your taxable income. So you’d also need an in depth knowledge of the tax system to understand exactly what is tax deductible and when.

Having a manual spreadsheet to record these transactions is fine if you have a financial background and know the legislation, or if you have an accountant guiding you. Alternatively you may use some form of accounting software. Again though the same rules apply, you’re likely to need an advisor if you don’t know exactly what you’re doing.

In the early days of starting out what should you do? Set up your own system by using a spreadsheet and save money? Or, invest in software and an established system that’s proven to work albeit at an added cost?

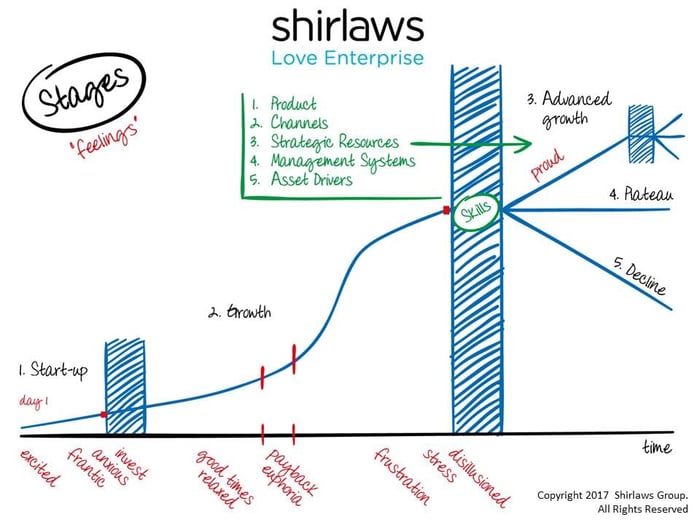

Consider the below example and diagram (the Stages Model, a concept originally developed by Shirlaws) to help inform your decision making in this area. Ultimately an accountant will be best placed to help you choose the option that’s best suited to your needs.

As an example, if you’re the owner of a tech start-up then it might seem obvious to go straight onto accounting software. After all you’re in the tech space! However, you might have raised finance (at the “1st brick wall”) courtesy of investors buying into your new idea for the market. Now you need to develop it over the next year or so and use these funds wisely before launching your solution.

It’s then a case of priorities and where to best allocate budgets in these early days. Thus the first year of your organisation's existence might be all about developing the brand and testing your new software/website product through market research. In this case a spreadsheet system could suffice for a period of time.

The reason being your business wouldn’t be generating any sales for the first twelve months or so. From a bookkeeping and accounting perspective the transactions taking place would be relatively simple because it would just be a case of recording all purchases. Why then spend much needed funds on accounting software at a time when you don’t need it yet?

Once your solution is on the market, you’d then expect the business to start making sales (“good times”). To start with the spreadsheet system might suffice, you’d simply add an extra column to reflect customer transactions. If however, you entered a period of rapid sales (“payback” moving into “fast growth”), you could soon outgrow such arrangements.

The vast number of transactions means the bookkeeping could become complex and you’ll get to a stage where you can no longer monitor it via a spreadsheet. There’s a risk you’d lose control of what’s happening in the business.

It’s as you enter this exciting phase of development that you’d need some form of automation in the form of software and credit control. That then allows you to maintain the rate of growth in your business and manage your cash position effectively.

Remember, the above is just an example. Ultimately there is no template answer to this question. All businesses are different. Any move to software will depend on your circumstances, the complexities of your sector and where your business is at in terms of trading.

Even if you take on an accounting software system, you’ll need to know what you’re doing in terms of the transactions otherwise:

Considering how crucial bookkeeping is to the production of your annual accounts, generating your tax return, and paying HMRC, it would very wise to seek the services of an accountant. That’s especially the case if your strengths and focus in the business aren’t around the finances.

If the relationship with your accountant develops, as it should from the start, then you’ll find their fees more than make up for the time, cost, and hassle of doing it all yourself. So choose your advisor wisely. Consider them to be both a very valuable investment, and intrinsic part of your business.

The content of this post was created on 23/09/2016 and updated on 21/02/2022.

Please be aware that information provided by this blog is subject to regular legal and regulatory change. We recommend that you do not take any information held within our website or guides (eBooks) as a definitive guide to the law on the relevant matter being discussed. We suggest your course of action should be to seek legal or professional advice where necessary rather than relying on the content supplied by the author(s) of this blog.

leave a comment -