The contrasting feelings of being totally overwhelmed by business growth and utterly underwhelmed by the lack of cash can leave you at a loss and concerned for the future of your organisation.

Too often we see growing businesses hit a financial crisis regardless of the quality of their service or swelling list of happy customers. It's almost always due to the detrimental and inevitable result of an inefficient credit control system. If you're seeing this trend develop in your organisation, or you're keen to avoid such a scenario, then you need to read on.

Late payments from customers can be the significant difference between the fine line of success and, failure. Sometimes payment is only a few days late, but this can mean weeks or even months before you receive it from when you delivered your product/service. It can cause serious cash flow issues and even throw your business’ future into peril - especially if you haven’t prepared for such delays.

Remember, you're investing money, time and effort to deliver your products or services to your customers. That's very likely to require a significant cash injection. Situations of uncertainty, whereby you have a multitude of late payments, will leave you in the horrid position of wondering how you will meet current and future financial commitments.

The solution however, is actually very simple. Putting a credit control system in place and investing the necessary time into this function will ease any cashflow strain and allow you to run the business more efficiently and effectively. Ultimately cash really is king!

Credit control is the system used by businesses to monitor and regulate the credit given to customers.

Typically, the longer your business allows customers to pay for your services, the more pressure you’re putting on yourself. How are you going to thrive if your business doesn't have cash coming promptly back in? You won't be able to invest in your employees, equipment, software or new premises because you either won't have the cash to hand to pay for it or, likely future cash coming in to service a loan.

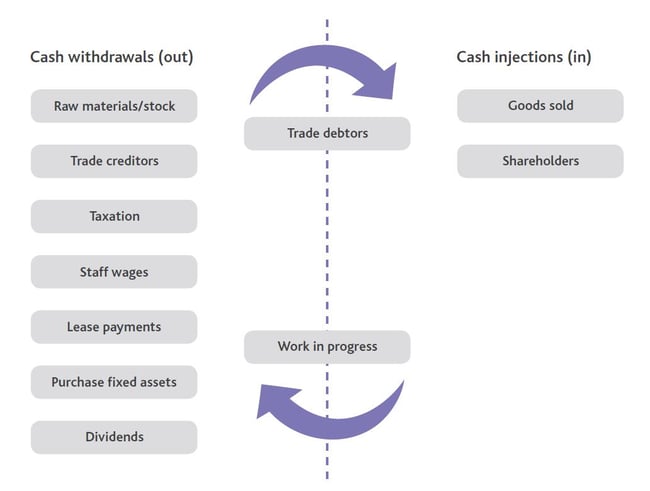

Customers who aren’t paying or, are paying continuously late, will result in more cash withdrawals than injections into your business. This causes your cash position to dwindle and it's alarming how quickly this can happen. It's why the act of balancing what's going out with what's coming in should be a fundamental component of your strategic decision making.

Typical procedures include, but aren’t limited to:

Typical procedures include, but aren’t limited to:Based on your discretion, you can apply individual credit terms to different customers. These can be implemented based on various factors including the customer’s credit rating and their historical promptness in paying previous invoices.

It’s understandable that when your business is reaching the growth stage your mind will be focused on maintaining/developing customer relationships and enhancing your product or service. However, to stay in business and grow in a sustainable manner requires you to monitor your cash position very carefully.

If your organisation is starting to show signs of poor cash management, then now is a good time to consider re-visiting the system and amount of credit you're extending to customers. Remember, a strong cashflow and avoiding unnecessary debts are vital ingredients of business success.

The content of this post is up to date and relevant as at 10/02/2017.

Please be aware that information provided by this blog is subject to regular legal and regulatory change. We recommend that you do not take any information held within our website or guides (eBooks) as a definitive guide to the law on the relevant matter being discussed. We suggest your course of action should be to seek legal or professional advice where necessary rather than relying on the content supplied by the author(s) of this blog.

leave a comment -