We presented on this recently, where we explored some of the different reliefs available, how they work and the tax deductions that can be achieved. Projects and even funding rounds undertaken can potentially qualify your growing business, your investors and even some employees for some significant savings.

We thought we'd share this with you highlighting some of the options that might be available and what you need to look out for.

Research & Development (R&D) tax relief takes place when a project seeks to achieve an advance in overall knowledge or capability in a field of science or technology that helps resolve scientific or technological uncertainties. Those engaging in such projects in the UK can benefit from a reduction in their corporation tax liability or in the event of a loss making business, receive a cash refund (credit).

As an example, if an SME makes a net profit of £400,000 after spending £300,000 on research, by submitting an R&D claim to HMRC the taxable profit could be reduced to as low as £10,000, thus saving approximately £74,100 in tax!

HMRC have advised that R&D is not just about white coat activities. We would therefore encourage anyone to consider all their business undertakings carefully to see if there is an opportunity to reduce corporate taxes.

The Patent Box allows companies to reduce their rate of corporation tax to 10% for profits specifically attributed to patents granted by the UK or European Patent Office. This includes EEA countries where the rules of patentability are similar to those in the UK. It also applies to other qualifying intellectual property rights such as regulatory data protection, supplementary protection certificates and plant variety rights.

The way this tax regime works is income from the patented product, or the product containing the patented item, is identified and the reduced rate of corporation tax applied to the profits associated with it. It can be very complicated and easy to misinterpret how much of your income is relevant to a patent which means you need robust accounting systems and controls in place to ascertain this source of revenue.

SEIS is a tax scheme for very early stage businesses, those less than 2 years old, to help them raise much needed funding. It works by reducing the risk for investors when an organisation is raising finance.

EIS is a similar scheme but allows larger funding rounds and applies to larger businesses than those that qualify for SEIS. The rules and benefits are a little different as such organisations carry a lower risk profile.

The rules for both businesses and investors are covered in an infographic we produced, how to find out if it's an SEIS or EIS investment. Be sure to review this.

To summarise, under SEIS an investor can fund up to £100,000 in any one tax year, for EIS this is £1 million. The government then provides up front income tax relief of up to 50% for SEIS, and 30% for EIS, of the money invested.

If the business succeeds and the investor makes a profit on the sale of those shares then that money is exempt from capital gains tax. If the business fails then they may be able to offset their loss against income tax.

This removes some of the risk of investments that go wrong while also improving the returns on those ventures that succeed. For business owners, it’s an attractive alternative source to raise finance.

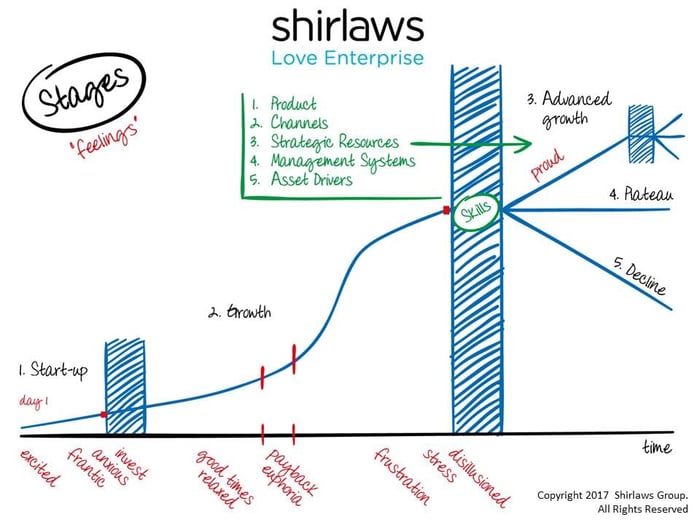

As you enjoy growth your brand and name will gain traction. This will in turn highlight both your business and your employees to larger competitors. It will likely form part of your next brick wall (see the stages model above, courtesy of Shirlaws) because it’s likely these corporates will try to poach your best employees with salary offers you’ll struggle to match as well as generous incentives.

Thankfully EMI share options could provide the answer. This scheme allows the option for selecting employees to be future shareholders and rewarding them for their work. It thus improves job satisfaction and productivity with the prospect of an eventual stake in the business.

Here’s how it works, your select staff are granted the option to purchase shares in the business at a set future date or event. A price known as the exercise price is set for the shares and fixed. At some point in the future, your employees then purchase their stake in your business, in the likelihood that the value of the shares has increased above the level originally set as the exercise price.

A further advantage for them is there is no income tax or national insurance payable on exercise. Also, the gain on potential sale of the shares is taxed at 10% through entrepreneurs’ relief. For business owners, EMI is an alternative form of remuneration that can potentially be used instead of a salary rise or bonus.

Both employer and employee benefit from a scheme like this.

The content of this post is up to date and relevant as at 31/05/2017.

Please be aware that information provided by this blog is subject to regular legal and regulatory change. We recommend that you do not take any information held within our website or guides (eBooks) as a definitive guide to the law on the relevant matter being discussed. We suggest your course of action should be to seek legal or professional advice where necessary rather than relying on the content supplied by the author(s) of this blog.

leave a comment -