When you first started your business you probably did your due diligence and prepared a business plan. But if you revisited that plan today, would it still be relevant to your business right now? The reality is that most business plans fail and you may be falling into some of the most common traps when it comes to yours.

Manoeuvering through your plan details can feel like a maze sometimes and you may start feeling like you'll never reach the finish line. Stay focused and positive because the hard work is worth the rewards. To help you through the process we've put together a handy infographic of 8 traps people often fall into, be sure to avoid these common mistakes.

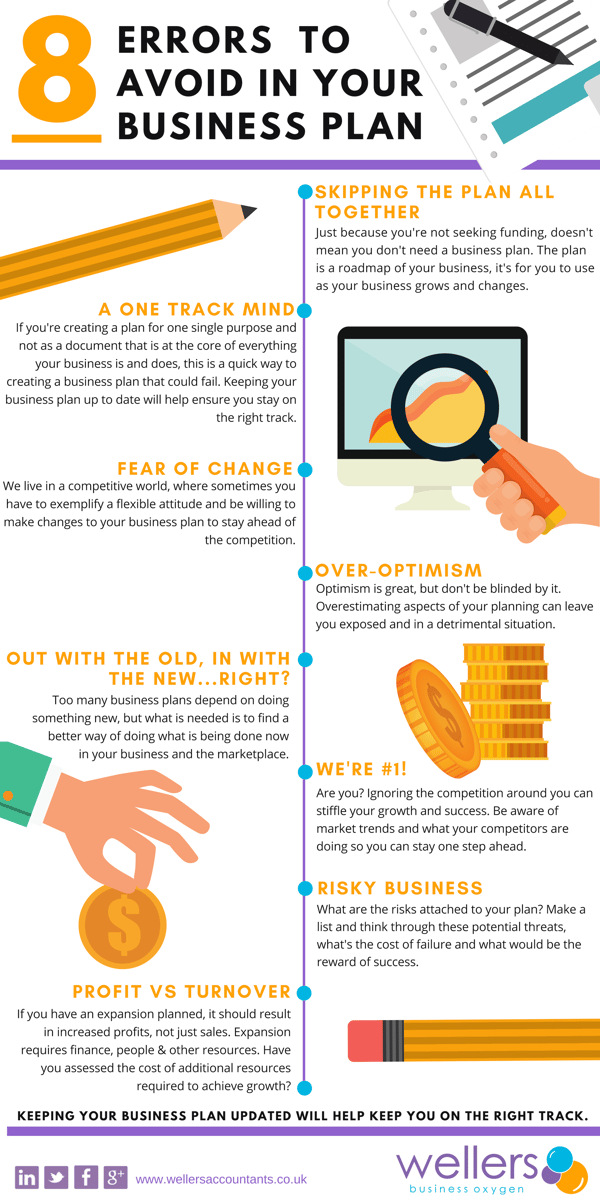

You might not be seeking financial help from a bank or investor and hence think, do I really need a plan or would it just be easier to grab the bull by the horns and get started? The short answer is “no”, this is not just a document to help you raise funds; it’s your roadmap off the back of your business idea.

We all get a little lost sometimes, isn’t it handy to have a map to help us out once in a while? That is exactly what a business plan will do for you, it will answer all the questions you’ll come across while starting and growing your enterprise.

We’ve described your business plan as being the roadmap, something to be referenced regularly and updated as your business grows. So if you’re creating it with a one track mind for a single purpose, say looking for funding, that's a potential route to failure.

It isn’t a one sided document with a single purpose, its at the core of your business and it’s important to make time to examine it; this is your chance to be critical and investigate if your current plan is still relevant to your enterprise.

We live in a competitive world, you may have come up with the next great idea, but competition will soon creep up behind you. This is why it’s important that your plan grows, develops and changes.

You need to stay focused on your business needs now, but remember that you may need to make changes to your approach in the marketplace to ultimately reach the goals you’ve set. This doesn’t mean overhauling the document every day; rather you should exemplify a flexible attitude when it’s in your best commercial interests.

Optimism is not a bad thing, when starting a business it’s a necessity because, as Winston Churchill once said, “Optimists see opportunities in every difficulty.” However, being over-optimistic when it comes to your plan can lead to some serious issues.

When you’re forecasting various aspects of your business, like sales for instance, overestimating the size of the market can be to your detriment. There will always be set backs that we may not be able to avoid, but with a healthy dose of realism we can plan for the bumps in the road by researching the market thoroughly to identify our strengths and opportunities.

We would all like to think that we are the best at what we do, and it will stay like that forever. We are 100% in control of the success of our business…right? You might just be the best at what you do, for now, who knows? If you ignore how your competition service their customers then you’ll never know how your business truly fairs in the marketplace.

Have you ever been in a race (or watched one) where the lead runner ends up being over taken by the competitor that’s been right on their heels the entire time? You can’t be watching your back, but you can observe your competitors and always try to be one step ahead when it comes to customer service and relationships.

If something isn't working, let’s just get rid of it and start afresh, right? Well, not necessarily. Too many businesses depend on doing something new to make a positive change, but the answer is actually in how we can find a better way of doing what is being done already.

If your plan is no longer working for your business just binning it isn’t the best option, think about why certain elements aren’t working for you and how you can improve on what’s there.

We all know a risk taker or two (have you ever had the urge to skydive?), but knowing what the risks are is one of the most important aspects of your business plan. What are the risks attached to the plan? Make a list of what these are and what they could cost your business, as well as, any rewards that you may gain by overcoming or avoiding them.

Are you focusing on profit, turnover or both? If expansion is planned for your business, increased profits should be an objective, not just sales. Are you prepared for an expansion which requires more finance and people? Do you have adequate resources?

A good business plan is not just about the final document, it’s about how you get there. The process of creating your plan will help you uncover the realities of your business. Once you have a successful one in place, keeping it reviewed and updated will help to keep you on the right track.

The content of this post is up to date and relevant as at 11/07/2018.

Please be aware that information provided by this blog is subject to regular legal and regulatory change. We recommend that you do not take any information held within our website or guides (eBooks) as a definitive guide to the law on the relevant matter being discussed. We suggest your course of action should be to seek legal or professional advice where necessary rather than relying on the content supplied by the author(s) of this blog.

leave a comment -